Current US Ports by Volume

As operation professionals and supply chain managers attempt to understand trends in demand, monitoring port volumes has become an essential practice. Maritime gateways are pivotal in global trade, handling 40% of the international freight value in 2022, according to the Department of Transportation. US Port volumes offer a reliable indicator for establishing trends over time.

Key statistics regarding US port volumes:

- In 2022, maritime gateways handled 40% of international freight value.

- From 2018 to 2020, the top 12 U.S. seaports managed approximately 46 million twenty-foot equivalent units (TEUs) of cargo.

- During 2021 and 2022, volumes surged to over 53 million TEUs due to the pandemic, leading to significant congestion and logistical delays.

- In 2023, volumes at the top 12 ports normalized to 46.67 million TEUs, slightly surpassing the 2019 record.

As the industry looks ahead to Q2 2024, tracking monthly data will be crucial in predicting future trends. Utilizing real-time supply chain data can provide insights into cargo volumes and historical trends by coast or specific ports.

Businesses must stay on top of tracking port volumes to anticipate and respond to changing demand. The fluctuations seen during the pandemic highlight the importance of agile supply chain strategies, and the need for adaptability in planning.

Companies should utilize real-time data and analysis to monitor cargo volumes and historical trends across various ports and coasts. By being proactive, companies can help identify potential bottlenecks and optimize operations to minimize delays.

Understanding the impact of external factors on port activity is crucial. These include global economic shifts, policy changes, and global threats impacting shipping lanes. Continuous investment in technology and data analytics will be key to enhancing visibility and decision-making capabilities.

Data and charts are from original content from Supply Chain Dive.

Decreased Consumer Demand and a Weak Economy Affecting all Modes of Freight

As the economy in the US slows down, and consumer demand decreases, there is a negative impact on freight volumes across all modes of transportation. Recent insights from The Supply Chain Exchange indicate that this economic downturn is causing havoc for carriers.

Companies must take this opportunity to review all aspects of their network and carrier contracts. By taking steps companies can successfully navigate through these times and ensure the resilience of their supply chain operations.

Three Impacts to Consider

1. Decreased Freight Traffic; The slowing economy in the U.S. Is likely to reduce the amount of freight moving through transportation channels like trucks, trains and planes. This could lead to capacity and higher shipping costs for logistics companies.

2. Price Instability; Due to demand freight rates may fluctuate unpredictably. Businesses could face varying shipping costs during times of surplus capacity making budgeting and forecasting more challenging.

3. Operational Streamlining; Reduced demand for freight should prompt companies to rethink their approaches to maintain efficiency. This could involve optimizing delivery routes consolidating shipments, utilizing technology for supply chain management and renegotiating freight contracts.

Two Ways to Challenge Your Operations

1. Enhance Freight Network Planning; Businesses should reassess their transportation network design to boost efficiency and cost effectiveness during downturns. This involves examining existing shipping routes and distribution centers to find ways to consolidate and optimize operations.

By analyzing their supply chain, companies can simulate scenarios and implement strategies that reduce delivery times and cut transportation expenses. These strategies may involve combining shipments into loads choosing more effective routes and exploring different modes of transportation to meet changing demand.

2. Renegotiate Freight Agreements; With the conditions leading to reduced freight demand, businesses have an opportunity to renegotiate their freight agreements. It's important for companies to thoroughly review their contracts paying attention to aspects, like pricing, fuel surcharges and service level agreements.

Holding discussions with carriers can result in much lower freight costs, taking back some of the increases they were hit with during Covid. By capitalizing on the market environment businesses can save significant freight costs.

One Final Thought

Given the slowdown in the economy and decreasing consumer demand its crucial for businesses to take a strategic approach in managing their freight operations. Companies should not just focus on cost cutting measures. They should also invest in long term resilience and efficiency.

While it may be the best time to renegotiate lower freight costs, companies must consider their broader supply chain and distribution network. Consider these questions:

- How can your business leverage these carrier challenges to better service your customers?

- Are you maximizing inbound and outbound freight and modes of freight?

- Are there more optimal inbound ports, outbound distribution points or carrier lanes that you should consider?

- Are there carriers that you should reconsider (i.e. regional small parcel carriers, etc.)?

Supply Chain by the Numbers

| 373 Million | Square feet of industrial space leased in the U.S. in the first half of 2023, an 18% decline from the same period last year, according to CBRE. |

| 66,295 | Loaded container imports into the Port of Oakland, Calif., in June, a 30.6% decline from last year and down 6.5% from May. |

UPS, Teamsters Agree in Principle to Changes with SurePost Delivery

UPS, through meetings with the International Brotherhood of Teamsters, has recently reached a tentative agreement to reduce the size of SurePost packages eligible for delivery through the U.S. Postal Service. This move aims to optimize operations and enhance efficiency in the final mile of package delivery. While specific details have not been disclosed, the agreement holds potential implications for both UPS and its customers.

According to Kara Deniz, spokesperson for the Teamsters Union, the tentative deal involves a reduction in the overall size of packages eligible for SurePost delivery. However, specific details regarding the revised size limits have not been disclosed at this time. Deniz did mention that the proposed changes would result in an increased proportion of SurePost packages being handled by regular package drivers within the Teamsters Union. These commitments from UPS aim to gradually redirect more SurePost packages to the bargaining unit's drivers over the duration of the contract.

Back to School Demand Signals Early Softness

The logistics industry often focuses on peak season expectations, but it's essential to also consider the back-to-school shopping season. Similar to holiday orders, this season typically spans from mid-July to early/mid-September. Shippers and logistics companies are currently discussing back-to-school logistics planning, which provides insight into the retail sector's expectations for consumer spending.

A deeper analysis of metrics is necessary to truly understand the future, beyond just looking at overall volumes moved during the back-to-school or peak season, per FreightWaves. Examining different verticals within the supply chain is crucial for accurately assessing consumer health. The supply chain's status is not a binary issue; it consists of various shades of gray. By examining consumer demand within specific product segments, companies can improve inventory management.

Drew Wilkerson, CEO of RXO, expects back-to-school orders to be similar to last year or slightly higher, particularly noting a rise in apparel orders. Technology orders also play a significant role as students return to full-time schooling for the second year following the COVID pandemic.

However, Paul Brashier, vice president of drayage and intermodal for ITS Logistics, highlights ongoing weakness across all retail aspects compared to the previous year, with a significant decline of 30%-35% in volumes of back-to-school goods. This decline is attributed to substantial inventories remaining in shipper distribution centers, impacting office supplies, clothing, and electronics.

Despite the overall decrease in volumes, high-end goods outperform discount goods in terms of import volume. This is due to discount retailers sourcing inventory from excess stock in U.S. distribution centers rather than relying on overseas suppliers as in the past.

Warehouse and Industrial Space Demand Shifts Away from Retailers

The U.S. warehousing industry is experiencing a fresh surge in a new market, coinciding with the decline of its previous major growth driver. Industrial real estate is increasingly being occupied by renewable energy companies, particularly those involved in the manufacturing of solar panels, electric vehicles (EVs), and EV batteries.

These companies are actively establishing new supply chains, resulting in a significant increase in leasing activities during the first quarter, per the WSJ. As demand from consumers and businesses rises and with the aim to compete for federal subsidies aimed at supporting the renewable sector, these companies are quickly securing warehouse spaces.

This growth is occurring as the consumer economy shifts its focus away from the rapid expansion of e-commerce. According to real estate firm CBRE, e-commerce companies leased a total of 4.7 million square feet in the first quarter, a significant decrease from the 13.7 million square feet leased during the same period the previous year.

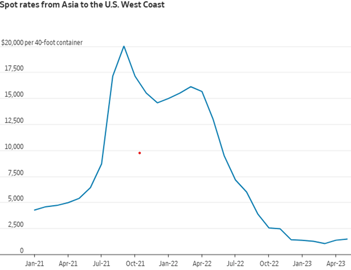

Container Shipping Profitability Creates Risk

The container shipping industry has swiftly transitioned from a state of prosperity to one of decline. The sharp drop in prices is leading major container ship operators to incur losses on previously profitable trans-Pacific routes, as reported by the WSJ's Costas Paris.

prices is leading major container ship operators to incur losses on previously profitable trans-Pacific routes, as reported by the WSJ's Costas Paris.

This is an alarming indicator for the sector as it gears up for its busiest period. As per the Freightos Baltic Index, the average daily freight charges from Asia to the U.S. West Coast via the Pacific now stands at approximately $1,500 per 40-foot container, a drastic decrease from over $14,000 last year.

The rate from Asia to Europe has also tumbled, currently at around $1,400 compared to nearly $11,000 the previous year. Despite the free-falling prices that marked the earlier part of spring seeming to stabilize, the rates for both these trading corridors are currently similar to those of 2019. With shipbuilders set to introduce more capacity into the market, shipping companies find themselves with little leverage in a container market increasingly dictated by the buyers.

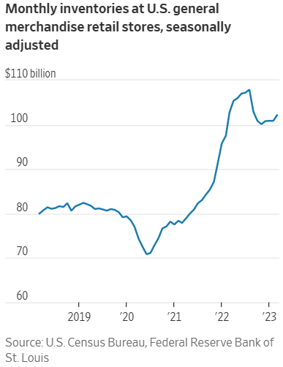

Major Retailers Taper Inventory Reduction Initiatives

Major retailers are concluding their inventory reduction initiatives that have exhausted distribution networks and crippled freight carrier revenues. Both Walmart and Target have recently indicated that their stock levels are healthy, as reported by the WSJ Logistics Report, a positive turn of events following a year that saw merchants reduce orders due to overcrowded warehouses and lagging consumer demand.

freight carrier revenues. Both Walmart and Target have recently indicated that their stock levels are healthy, as reported by the WSJ Logistics Report, a positive turn of events following a year that saw merchants reduce orders due to overcrowded warehouses and lagging consumer demand.

Target's executives suggest that the era of overstocking is behind them, and the focus now shifts towards introducing new merchandise into stores for the autumn and holiday seasons. This shift would be a welcome change for freight carriers, who have been anticipating a restocking phase to uplift the currently suppressed cargo volumes.

Some operators have reported that customers are indicating that inventory reduction is essentially complete, although new consignments are not yet being dispatched towards distribution centers. The extent of restocking, however, is still uncertain: Target mentions that its strategy will center around "inventory efficiency."

Shopify Sells Fulfillment & Logistics Along with 6 River Systems

Flexport, a San Francisco-based freight forwarder, has acquired Shopify's fulfillment and logistics operations, expanding its services to include warehousing, packing, and shipping for Shopify's merchants. The acquisition will enable Flexport to establish itself as a direct competitor to Amazon's fulfillment services. This move is part of Flexport's strategic plans to expand its offerings and capitalize on the growth of e-commerce during the pandemic.

The combination of Flexport's technology platform and Shopify's logistics capabilities will allow merchants to simplify and optimize their supply chain operations, so they can focus on designing and selling great products. Shopify's fulfillment network has grown to over 20 fulfillment centers across the U.S. and Canada, with the ability to ship to 99% of the U.S. population within two days. With the rise of e-commerce over the past year, Shopify has seen increased demand for reliable and affordable fulfillment solutions.

Flexport's revenue grew 56% in 2020, despite the challenges posed by the pandemic. According to eMarketer, e-commerce sales in the U.S. grew by 32.4% in 2020, reaching a total of $794.50 billion. With the continued growth of the e-commerce market, this strategic move by Flexport will likely benefit both companies and their customers, as they seek to streamline supply chain operations and provide reliable and affordable fulfillment solutions.

According to the WSJ, the sale includes warehousing automation firm 6 River Systems, effectively ending Shopify’s attempt to stand up its own logistics fulfillment operation alongside the e-commerce sales technology platform it offers merchants.

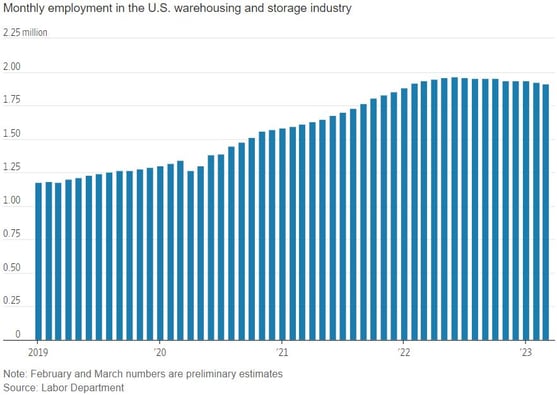

Warehouse Jobs Fall to a 15 Month Low

Based on the latest data, warehouse jobs have recently reached their lowest level in 15 months. This trend is driven by several factors including increased automation, labor shortages, and a shift in business focus towards value-added activities within the supply chain.

Between February and March, U.S. employers eliminated 11,800 warehouse and storage positions, based on the preliminary jobs report from the Labor Department, which has been adjusted for seasonal variations. Since June, warehousing companies have cut close to 50,000 jobs, as retailers with excessive inventory began scaling back due to uncertain consumer demand, according to WSJ.

Despite this overall decline, certain areas within the warehouse sector continue to grow, particularly e-commerce. However, to adapt to the labor challenges, companies have been investing in new technologies to optimize fulfillment and reduce labor costs.

Many companies are utilizing automation, robotics and artificial intelligence to automate repetitive tasks, enabling their human workforce to focus on more complex responsibilities. In addition, businesses are increasingly turning to third-party logistics providers for their expertise and resources, helping them navigate the rapidly evolving industry landscape.

What does this mean, and what to do about it:

- Even though there has been a decrease in jobs, many companies are still struggling to find qualified, reliable labor. Warehouse optimization and efficiency still need to be primary drivers for companies.

- Companies must continually evaluate automation and technology to determine how and where labor costs can be reduced or eliminated.

- For many companies, automation allows them to focus on developing core staff. Additionally, companies can remove repetitive tasks and allow workers to focus on more meaningful tasks.

Inventory Gluts Aren't Ending Soon, Negatively Affecting Profits

Excess inventories in warehouses are creating pressure on the bottom line of many companies, and associated storage costs may not ease up this year, a recent CNBC Supply Chain Survey showed.

More than a third of the respondents anticipate inventories to return to normal in Q3 2023, while an equal percentage expect the glut to persist until 2024. The survey also revealed that 20% of the excess inventory in warehouses is non-seasonal in product nature, leading to challenges for logistics experts.

The survey showed that slightly over a quarter (27%) of the participants are selling on the secondary market, as elevated storage prices are impacting the company's bottom line. The “other” category, including rent and labor, was the second-biggest category affecting inflationary pressures, with almost half of the respondents stating so.

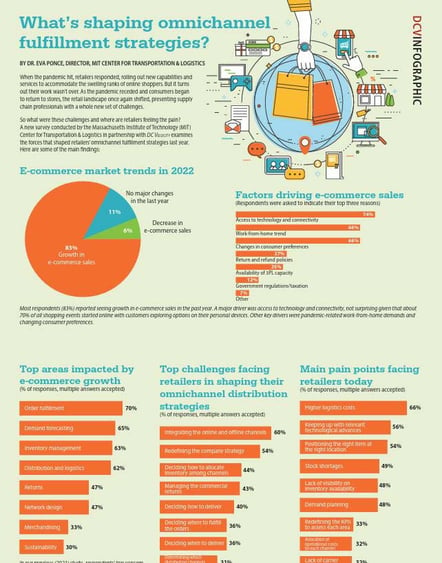

What’s shaping omnichannel fulfillment strategies?

The Massachusetts Institute of Technology (MIT) Center for Transportation & Logistics conducted a survey in partnership with DC Velocity to analyze the factors that drove retailers' omnichannel fulfillment strategies in the previous year.

The survey results provided insights into the key trends that influenced retailers' decision-making processes, such as the impact of the COVID-19 pandemic on online shopping and the need for greater supply chain agility. Additionally, the study found that retailers had to invest in new technology and collaborate with their supply chain partners to enhance their omnichannel capabilities.

Overall, the survey sheds light on the challenges and opportunities faced by retailers as they adapt to the evolving retail landscape.

FedEx Announces Layoffs as Volumes Decline

This week FedEx announced its quarterly earnings, and the results weren’t good, further highlighting the decline in shipping volumes. Partly due to the decline in ecommerce volumes, FedEx stated that it will cut 25,000 workers by May of this year. These efforts are to try and streamline costs in efforts to boost profitability.

This is on the heels of layoffs in the broader freight markets. Per the WSJ - trucking, warehousing and parcel-delivery companies cut a combined 16,900 jobs in February, following a drop of 2,200 jobs in January, according to seasonally adjusted preliminary employment figures released Friday by the U.S. Bureau of Labor Statistics.

What does this mean, and what to do about it:

- This comes at a time when UPS is beginning deep union negotiations to avoid a strike, while FedEx is looking to improve their on-time delivery, etc. This can certainly lead to uncertainty in carrier delivery should UPS not negotiate a deal with the union.

- Take this opportunity to determine whether additional costs that can be negotiated out of your current carrier contracts, also understand how regional carriers can potentially reduce risks with UPS or FedEx.

Supply Chain by the Numbers

| 184,189 | Loaded container imports into Georgia’s Port of Savannah in February, in 20-foot equivalent units, down 16.4% from last year and the lowest monthly level for imports since June 2020, per WSJ. |

| $1,071 | Average spot price to ship a 40-foot container from Asia to the U.S. West Coast the week ending March 3, lower than at any point in 2019, according to Freightos. |

St Patrick's Day Consumer Retail Spending

According to the NRF, consumers are sparing no expense to go all out for the holiday this year. Consumers plan to spend a total of $6.9 billion — $1 billion more than last year — or an average of $43.84 per person.

And men are ready to spend more than anyone else. For as long as NRF has tracked the holiday, men have spent substantially more than women on St. Patrick’s Day festivities. This year, they are spending $48.71, almost $10 than women’s $39.15. What are they spending it on? Well, women buy more of every category than men except one — beverages. Sláinte, lads!

What does this mean, and what to do about it:

- Outlook reflects a consumer that is still holding up the economy in certain segments.

- Grab a green beer, or favorite non-alcoholic beverage, and enjoy some time away from the office with friends or family!

Inside Look at Freight & Transportation

In this industry, we have always viewed the freight and transportation side of the business as a view into economic health, and a barometer as to whether things are headed. Changes in shipping volumes, whether raw materials or finished goods, are felt in the transportation industry long before economic indicators begin pointing to a trend.

We are in a period where those changes are the transportation side are visible, and the outlook isn't favorable for shippers or carriers.

From the carrier's side of the ledger

- Retail inventories are building, forcing many companies to begin planning markdowns.

- Outlook form major retailers such as Walmart and Home Depot provided soft or weakened guidance from the consumer perspective.

- Consumers have the lowest savings rate since 1960, leading many to speculate the consumer can't prop up the economy much longer.

- According to TI, Driver wages, insurance, equipment and truck parts cost more than a year ago. For example, Trailers that used to be $20-25K now cost $60-80K.

- High interest rates make financing large capital expenses, like truck purchases, even more difficult.

- Additionally, freight rates have fallen nearly 40% since January 2022, reducing carrier income significantly. Combined with higher costs, this has led to the most carriers going bankrupt in

2022 since 2008. 2023 will be worse.

Carrier Forecasts for Q1/Q2 2023

- Small parcel capacity constraints are projected to begin to subside in 2023, as carriers continue to address challenges.

- Small parcel carriers continue to extend peak surcharges beyond peak season. Select surcharges are now in effect “until further notice” with UPS renaming them “demand surcharges.” This is not expected to change.

- The record rate increases, UPS at 6.9% up from 5.9% in 2022, comes at a time when shipping volumes are softening. There will be a point at which shippers will be motivated to contractual discounts and carriers will become more competitive for that business.

- The lead up to the UPS/Teamsters contract negotiations, and the results of the contract negotiations, will have a direct impact on how UPS prices contracts.

- LTL carriers see the first half of 2023 as being potentially soft. Many are seen as lowering costs and streamlining operations instead of lowering rates, as of now.

- Many LTL carriers are taking loads they wouldn't have otherwise accepted previously, this is expected to continue for the first few quarters.

- Carrier bill counts are down. However, LTL carrier rates will not decrease drastically due to less

fragmentation and more pricing power in the LTL market versus the TL market.

What does this mean, and what to do about it:

- In these market conditions, it is critical to at least get a quick gut check to see what challenges should be address, and what opportunities exist in your supply chain.

It's as easy as just a simple discussion with FCBCO & TI to understand your shipping characteristics and volumes. From there, we can share our perspectives.

Supply Chain by the Numbers

| 4.3 | Average number of days containers waited to move by rail from the ports of Los Angeles and Long Beach, Calif., in January, the shortest wait time since January 2022, per WSJ. |

| 237,705 | Intermodal units moved by rail the week ended Feb. 18, down 8.8% from 2022, according to the Association of American Railroads, per WSJ. |

| $73.9 Billion | Total value of North American transborder freight that moved by truck in December, down 6% from November and up 5.8% compared with December 2021, according to the Bureau of Transportation Statistics, per WSJ. |

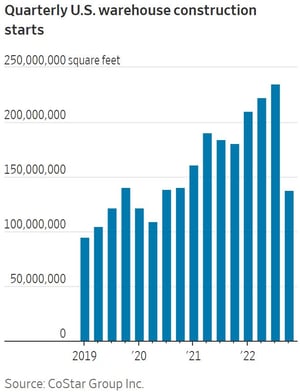

New Industrial Construction Fell 24% in 4th Quarter

With high interest rates, it should be no surprise that investors and developers have slowed the rate of new industrial construction, including warehouses and distribution centers. This according to WSJ and Costar in a recent report, adding "Developers began building about 137 million square feet of new warehouse space, the lowest amount of new space to start construction in a quarter since the beginning of the Covid-19 pandemic."

With high interest rates, it should be no surprise that investors and developers have slowed the rate of new industrial construction, including warehouses and distribution centers. This according to WSJ and Costar in a recent report, adding "Developers began building about 137 million square feet of new warehouse space, the lowest amount of new space to start construction in a quarter since the beginning of the Covid-19 pandemic."

With the average large scale distribution center taking roughly 13 months to complete, this is certainly going to have a negative impact on future distribution centers in Q2 2024. This comes as existing occupancy rates remain extremely high. Pushing lease rates and 3PL storage costs to some of the highest levels encountered by retailers.

What does this mean, and what to do about it:

- Companies that are considering a facility move, or expansion to the current number of DCs, should consider expediting the decision making process. This would include any distribution network analysis studies, or the potential use of 3PL options, as available space will impact most models.

- Continue to find ways to optimize the current facility from a utilization and capacity perspective. Focus on getting the most out of the current facility, without risking the flow of goods, safety or efficiency. A facility that remains above 85% for extending periods of time is considered "full".

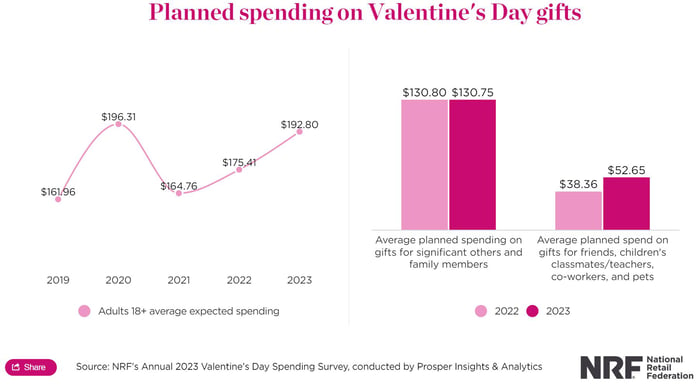

Valentine’s Day Spending to Hit Nearly $26 Billion

According to the NRF, Valentines Day sales were expected to hit nearly $25.9 billion this year, up from $23.9 billion. The NRF states, "More than half (52%) of consumers plan to celebrate and will spend an average of $192.80. This is up from $175.41 in 2022, and the second-highest figure since NRF and Prosper started tracking Valentine’s Day spending in 2004. "

Of the $17 increase in per-person spending, $14 comes from gifts for pets, friends and co-workers, along with classmates or teachers.

DISTRIBUTION & SUPPLY CHAIN INSIGHTS - WEEK of 2/1315 SECOND RECAP- Bloated Retail Inventories Will Continue to Drive Inflation |

Bloated Retail Inventories Will Continue to Drive Inflation

There has certainly been a significant focus on interest rates and inflation, not just in the US but abroad. And rightfully so, as consumers have seen escalating price increases across all major categories. While some of the latest economic data shows some areas plateauing, there are still supply chain pressures that will keep pushing costs on to consumers.

Even though ocean freight has dropped in cost, and trucking carriers have excess capacity, retail inventories have been piling up. As inventory levels remain elevated, or in some cases continue to climb, there is less available warehouse space to store them.

This problem has led many companies to look at everything from keeping inventory inn containers at ports, to outsourcing warehouse operations to ease the burden. With decreased warehouse availability and options, retailers are paying the highest storage costs in recent history.

These costs will inevitably passed onto the consumer, furthering inflation fears.

What does this mean, and what to do about it:

- Companies must continually scrutinize forecasts and make adjustments as quickly as possible within their supply chain. Challenge all aspects when the forecasts drops - i.e., can you cancel or modify existing POs, how quickly can you liquidate or markdown inventory to relieve storage pressures and cost.

- Consider all 3PL options if you are in need of offsite storage. There are significant cost differences in long term versus short term storage. What you are storing will also have direct impacts on 3PL storage costs.

- Scrutinize your internal supply chain storage facilities, ensure that you are optimizing warehouse bin and storage locations throughout. Identifies areas where you can recapture storage space. This should include reprofiling locations to maximize cube utilization.

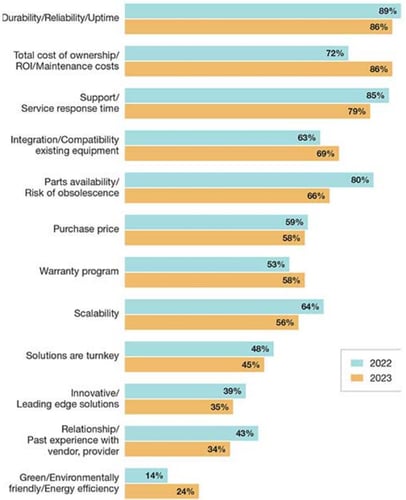

Where and How Companies Plan to Invest in Automation

Automation continually is improving and becoming more affordable for a wide range of businesses. In a recent study conducted by Modern Materials Handling (MMH), shows some slight declines in how much capital companies are planning to invest in automation.

According to MMH, "The average estimated spending level came in at $1.57 million, down from a $2.02 million average last year, and almost identical to the $1.579 million average two years ago."

Here is how respondents the importance of the each of the following when evaluating automated solutions.

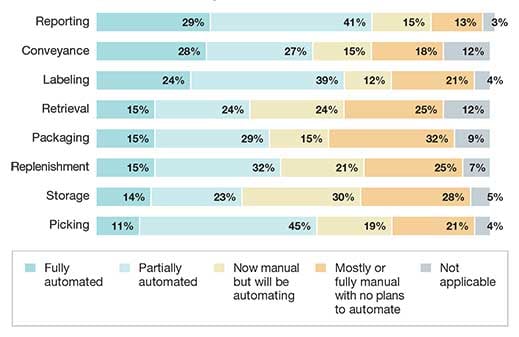

The following depicts where investments are being made within the operations.

What does this mean, and what to do about it:

- While the planned level of investments is down from a wide range of companies, it potentially opens the door for those looking to make additional investments. If investments drop, many vendors will be more aggressive with service offerings and investment required.

- This environment is a great opportunity to understand where and how automation and technology could benefit your operations.

- Understand where the opportunity is to reduce labor costs in using automation and technology.

Consumer Spending Remained Strong in January

One of the bigger surprises this week was the strength of consumer spending. Retail sales for the month increased 3%, compared with expectations for a rise of 1.9%. According to CNBC, On a year-over-year basis, retail sales increased 6.4%, which was exactly in line with the consumer price index move reported Tuesday.

In speaking with many retail clients, the results have been mixed. There are a significant number of retailers that have seen sales pull back to being inline with previous, pre-pandemic forecasts. This has created challenges, as noted above, regarding bloated inventory positions, etc.

There still do remain many strong, growth oriented retailers - some of these resilient categories is in luxury goods.

What does this mean, and what to do about it:

- As noted above, quickly identifying changes in purchasing and customer demand must be reflected in the forecast as quickly as possible.

- Consider how more robust vendor compliance programs can help streamline your operations.

DISTRIBUTION & SUPPLY CHAIN INSIGHTS - WEEK of 2/6

Industrial and Warehouse Space Still at a Premium

At the end of Q4, the market for available industrial and warehouse properties had eased a bit. According to a CNBC report, warehouse storage rates on a national level remain elevated. Fortunately the rates seem to have plateaued, at least for the current period, with no rise in rates quarter over quarter in Q4 2022. Stating, "Even as supply chain inflation slows, warehouse rates are high because there is a lot of inventory, which leaves less available space. The price for that space is sold at a premium. ".

Even in Richmond VA, headquarters of F. Curtis Barry & Company, the "...combined overall industrial market occupancy has slightly decreased to 94% in Q$ 2022", according to Porter Realty. This is down from 95% in Q3 2022. An additional 6 million square feet of new industrial construction underway. Asking rents grew by about 11.7% by EOY 2022, with 2023 on pace for 7.7% increases.

What does this mean, and what to do about it:

- With even markets like Richmond in tight availability, it is important to focus on maximizing warehouse capacity and utilization of the existing facilities in your supply chain.

- Perform a warehouse operations assessment to ensure that the existing operations are as finely tuned as possible.

- With landlords still firmly in control, and 5+ year leases being the normal, consider the benefits of 3PLs in your supply chain.

Freight Capacity Eases & UPS Teamsters Agreement

Freight still remains front and center for most supply chain professionals. According to most supply chain and transportation analysts, there is capacity available in all modes of transportation, and carriers are open for business. Carriers are seeking to add volumes to their networks and are willing to negotiate rates to secure the volumes.

Especially concerning to retailers, and ecommerce companies, all eyes are on the current UPS negotiations with the Teamsters and its 340,000 UPS workers. UPS President Carol Tome stated that a "win-win-win" agreement would be reached prior to the end of July.

What does this mean, and what to do about it:

FTL, LTL and small parcel carriers all have additional capacity:- As most have missed their forecast for volumes, they are willing to negotiate rates, its time to understand what carrier options exist for your business.

- If your business is concerned with a potential UPS strike, now is the time to negotiate with FedEx and regional carriers for small parcel volumes. If a work stoppage occurs with UPS, it will be too late to shift packages.

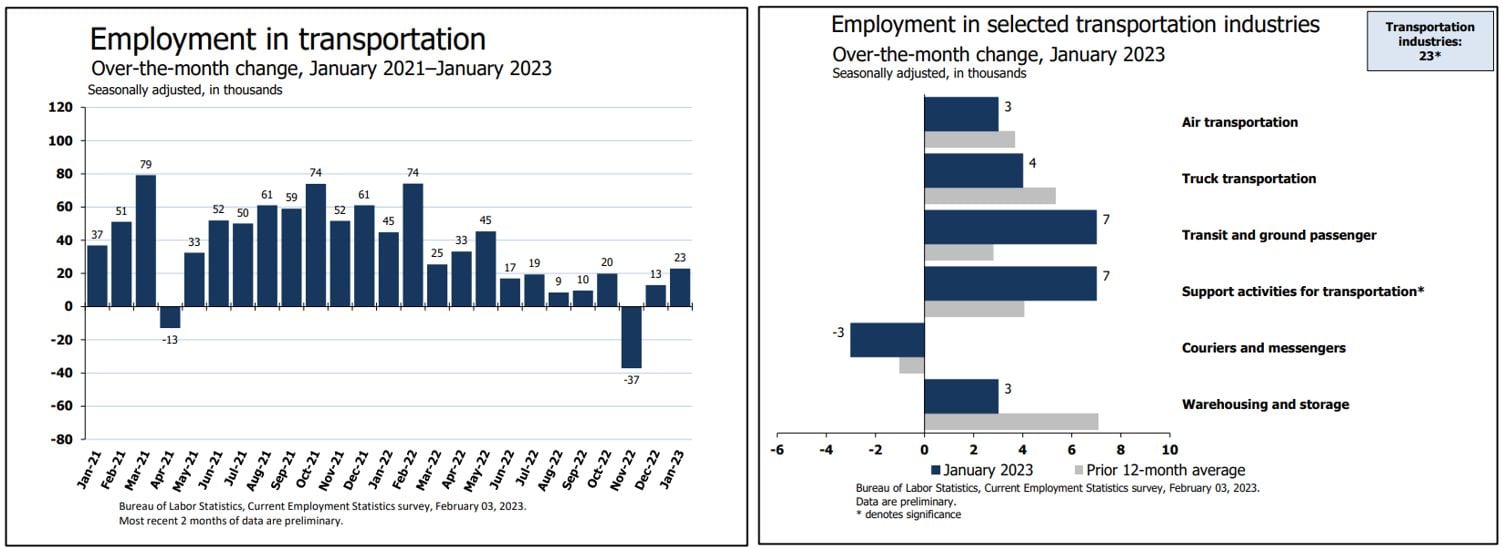

Warehouse and Transportation Adds 23,000 Jobs Last Month

At this point, distribution professionals could practically forecast the monthly jobs report themselves. According to the Bureau of Labor and Statistics, the warehousing and transportation industry added 23,000 jobs, which is in line with the 2022 average. The most recent data points to roughly 1.9 job openings for each unemployed individual.

What does this mean, and what to do about it:

- Labor remains a top concern for most distribution professionals, companies must ensure that facilities are running at optimal performance to drive down labor costs, consider an operational assessment.

- Ensure that you are managing warehouse labor appropriately, given your management objectives and customer expectations.

- Understand how automation and technology can reduce your dependency on labor in your warehouse operations.

SHARE